Emergency Fund vs Insurance: Why You Need Both (Not One)

Two Crutches, One Walk: Understanding Your Safety Net Picture your financial life as a long trek through the Himalayas. One pole in your hand is insurance—it shields you from sudden falls and dangerous cliffs. The other pole is your emergency fund—it supports you on uneven ground and unexpected twists. Drop either pole, and the trek becomes risky, tiring, and frightening. Many professionals lean on just one pole. Some believe a large emergency fund removes the need for insurance; others feel a hefty term or health policy is enough. Both assumptions leave dangerous gaps. What an Emergency Fund Really Does Definition A cash reserve covering 6–12 months of essential living costs—rent or EMI, groceries, utilities, school fees, transport, basic healthcare. Purpose Where to Park It Key rule: Instant access, minimal risk. What Insurance Actually Covers Term Life Insurance Protects the family’s lifestyle and goals if the breadwinner passes away. Sum assured should equal 15–20× annual income plus outstanding liabilities. Health Insurance Covers hospitalisation costs, surgeries, and long‐term treatments. Adequate cover for a metro family is often ₹10–15 lakh plus a top‐up. Critical Illness & Disability Riders Provide lump‐sum payouts if diagnosed with major illnesses or facing loss of income due to disability. What Insurance Doesn’t Do Why One Cannot Replace the Other Scenario Emergency Fund Insurance Who Saves the Day? Job loss for 5 months ✅ Yes ❌ No Emergency Fund ₹4 lakh knee surgery ❌ Partial (may drain fund) ✅ Yes Health Insurance Car gearbox failure ₹70,000 ✅ Yes ❌ No Emergency Fund Cancer treatment ₹20 lakh ❌ No ✅ Yes Health + Critical Illness Breadwinner’s death ❌ No ✅ Yes Term Insurance Shift to new city, deposit + rent ✅ Yes ❌ No Emergency Fund Both pillars complement; neither substitutes the other. Common Myths That Sabotage Financial Security Building Your Two‐Layer Safety Net: A Step‐by‐Step Plan Step 1 – Calculate the Right Numbers Item Formula Example (Metro Family) Emergency Fund 6–12 months of basics ₹60,000/month × 9 months = ₹5.4 lakh Term Cover (Annual income × 20) + liabilities ₹18 lakh × 20 = ₹3.6 crore Health Cover Family size + city cost ₹10 lakh base + ₹25 lakh top‐up Step 2 – Build the Emergency Fund First Step 3 – Buy Adequate Insurance Immediately Step 4 – Review Annually Step 5 – Keep Them Separate Real‐World Examples Case A – Emergency Fund Saved the Day Neha, a Mumbai marketing manager earning ₹1 lakh/month, built an ₹8 lakh emergency fund. When her company downsized, she remained jobless for four months. Not a single EMI defaulted, and she rejected the first low offer, waiting for a better fit. Outcome: Career intact, confidence high. Case B – Insurance Prevented Wealth Destruction Ravi, a 38‐year‐old tech lead, bought a ₹15 lakh health cover and ₹50 lakh top‐up. A sudden cardiac event cost ₹18 lakh. Insurance paid the bill; the family’s savings and future goals stayed untouched. Case C – Missing One Pillar = Financial Shock Arun, 45, had ₹6 lakh emergency savings but no term cover. He passed away in an accident. His wife received only the savings and small PF, far below the ₹1 crore needed for children’s education and home loan. One missing pillar collapsed the entire plan. Frequently Asked Questions Q1: Can I reduce insurance once my emergency fund is big?No. Insurance handles high‐cost, low‐frequency events. The fund tackles moderate‐cost, high‐frequency events. Keep both. Q2: How liquid should the emergency fund be?Access within 24 hours—savings account with sweep FD or liquid mutual fund. Avoid locking it for >7 days. Q3: Should I invest the fund for higher returns?Return of capital beats return on capital here. Prioritise safety over yield. Q4: What if premiums feel expensive?Compare pure‐risk online term plans; they’re affordable. For health, choose a higher deductible plus top‐up to reduce cost without sacrificing coverage. Action Checklist (Download‑Friendly) Closing Thought: Freedom Lives in Preparation Financial freedom isn’t merely about high returns or bigger salaries. It’s about sleeping well tonight, knowing two protections stand guard: Together, they let you pursue ambitions, invest aggressively, and enjoy life’s rewards without fear. Start building your twin safety net today. Future‐you—and your family—will thank present‐you for the calm, confidence, and choices you secured.

Why Most Indians Struggle With Wealth Despite Income

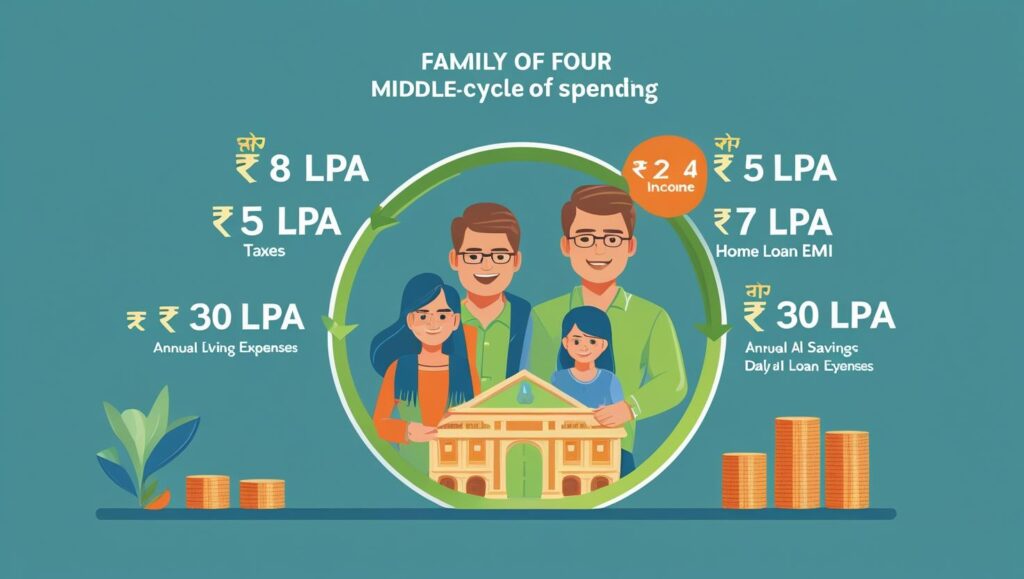

Why Most Indians Struggle with Wealth The Truth Hidden Behind Pay Slips: In India, even high-income professionals often feel financially stressed. Individuals earning ₹15–20 lakhs a year report feeling broke mid-month. Despite strong salaries, they’re caught in debt cycles, under-saving, and constantly firefighting financial issues. This disconnect between income and financial well-being isn’t rare. It’s widespread and solvable. Income ≠ Wealth A high salary is not the same as financial freedom. Think of income as water from a tap and wealth as the water collected in a tank. If the tank has holes—like poor financial habits, emotional spending, and lifestyle pressure—the tank never fills. Wealth isn’t about how much you earn. It’s about how much you keep, grow, and protect. Seven Reasons Why High Earners in India Stay Broke 1. Lifestyle Inflation With every raise, people upgrade their lifestyle: Bigger car Larger home with higher EMIs Expensive gadgets Fine dining, more frequent vacations This upgrade feels deserved, but it consumes the extra income and prevents wealth accumulation. Expenses grow at the same rate—or faster—than income. 2. Lack of Financial Education Schools and colleges don’t teach personal finance. Most people learn about money through trial and error or from friends and family. This leads to: Poor savings discipline Wrong insurance products Overexposure to risky investments No budgeting or cash flow planning Without knowledge, even high earners make beginner-level financial mistakes. 3. Overdependence on Parents’ Advice Many working professionals rely on their parents for financial decisions. While well-intentioned, older generations often recommend outdated products like endowment plans or FDs. Today’s financial landscape requires updated thinking—SIPs, term plans, asset allocation, and tax efficiency. Financial independence includes independent financial decision-making. 4. Absence of Financial Goals Most professionals do not have clear, written financial goals. Without goals, investments are reactive: Random SIPs Last-minute ELSS purchases for tax Taking advice from unqualified sources Clear goals bring purpose to every rupee saved and invested. 5. Blind Faith in Corporate Benefits Health insurance, EPF, and group term cover are helpful, but not enough. These benefits disappear if you switch jobs, take a break, or retire early. Relying solely on corporate perks leaves you underprepared for emergencies and long-term security. 6. Peer Pressure & Social Comparison Comparison drives unnecessary financial decisions: Buying a car because a friend did Signing up for premium club memberships Borrowing to fund lifestyle choices This leads to stress, low savings, and poor asset growth. Matching others’ lifestyles doesn’t help you reach your personal wealth goals. 7. Lack of Financial Communication In many households, couples avoid talking about money. Parents don’t involve children in financial decisions. Professionals don’t seek advice or clarity. Avoidance leads to financial misalignment within families and missed opportunities for smarter planning. Shift from Income-Based Living to Wealth-Based Living The solution lies in shifting focus: From earning more → to managing better From spending emotionally → to spending intentionally From hoping → to planning High income is a strong start. But sustainable wealth requires discipline, structure, and action. Seven Habits That Build Real Wealth 1. Pay Yourself First Before spending on anything, save a fixed percentage of your income. Automate investments. Build the habit. This one move ensures consistent wealth growth. 2. Live Below Your Means Wealthy people don’t overspend—even when they can. Choose peace over pressure. Choose future freedom over present comparison. Spend less than you earn. Always. 3. Have Written Financial Goals Goals give direction to money. Set clear goals for: Emergency fund Retirement Children’s education Home purchase Passive income Break them down into amounts, timelines, and monthly contributions. 4. Start Investing Early The earlier you start, the more compounding works in your favor. Even small SIPs, when started early, grow into crores over 20–30 years. Don’t wait for perfection. Start with what you have. 5. Get Insured the Right Way Take term insurance to protect your family. Have personal health insurance outside your job. Avoid mixing investment and insurance. Financial security comes from being prepared for life’s uncertainties. 6. Track and Review Finances Monthly Use a spreadsheet, app, or pen and paper—just track. Check: Income vs. expenses Net worth growth Savings rate Investment performance Monthly reviews help you course-correct before problems arise. 7. Keep Learning Read. Attend webinars. Ask questions. Learn about: Mutual funds Tax planning Debt management Retirement strategies Financial literacy compounds just like money. Reflect on These Questions Use these to assess your financial health: Do I save before spending—or save what’s left over? How many months of expenses can I survive without income? Have I calculated my retirement number? What financial habits do I want to pass on to my children? Am I building assets—or just collecting liabilities? Conclusion: Wealth Is Built, Not Earned India is full of salaried professionals and business owners with strong incomes but low wealth. The difference-maker isn’t how much they earn. It’s how they think and behave with money. Wealth is built through intention, discipline, and a repeatable system. No matter your background, degree, or city—you can start building peaceful wealth today. The goal isn’t to look rich. The goal is to live free. And the journey begins with the decision to take control.

The 5 Common Reasons Why Most People Fail at Budgeting (And How to Succeed)

💡 Budgeting is one of the most Googled financial terms, but also one of the most abandoned resolutions. Everyone starts with energy. Few stay with discipline. Most quietly quit by Week 2. But why? Why is it that despite knowing we should budget, we don’t? That’s exactly what we’ll unpack today — in real talk, Indian life context, and with solutions that stick. Why Budgeting Sounds Good but Fails Fast Let’s be honest. “Budgeting” feels like: No one likes that energy. We think budgeting = restriction. But the truth is… 🚫 The 5 Common Reasons People Fail at Budgeting ❌ 1. They Overcomplicate It Spreadsheets with 28 categories. Colour-coded apps. Daily logging. It starts to feel like managing a company’s accounts, not your own life. Budgeting shouldn’t feel like homework. It should feel like clarity. ❌ 2. They Budget Based on Ideal Life, Not Real Life “From now, I’ll eat out only once a month.” “My fuel cost will be ₹1000 max.” “I’ll save ₹30,000 every month.” 🙄 This is budgeting based on motivation — not behaviour. When reality hits, you overspend, feel guilty, and drop the whole thing. ❌ 3. They Track After, Not Before Most people react to expenses. “Let’s see how much I spent last month.” That’s called expense tracking, not budgeting. Budgeting is a plan for your money before the month starts, not a post-mortem. ❌ 4. They Don’t Include Joy Here’s a controversial truth: Any budget that doesn’t include fun… will fail. You need a guilt-free “fun allowance.” Even if it’s ₹1,000 a month for pani puri, chai, or a date night. ❌ 5. They Budget Alone in a Family System Especially in Indian homes, we often budget individually, but spend money collectively — spouse, kids, parents, relatives. If your partner doesn’t know the plan, If your family doesn’t align with goals… You’ll constantly feel off-track. 💥 The Big Mindset Shift: Budgeting = Buying Freedom Budgeting is not about punishment. It’s not about becoming “cheap.” It’s about this: “I tell my money where to go — instead of wondering where it went.” Budgeting is like giving your money a job. Every rupee should have a role: Suddenly, money becomes your team. You’re the CEO. The rupees are your employees. You assign. They perform. 🧠 The Shiv Budgeting Method: Freedom Budget Blueprint™ Let’s simplify your life, Shiv-style. Here’s a simple, 3-part budgeting system I use with my students: ✅ Step 1: Split Into 3 Broad Buckets Forget 25 categories. Use this clean formula: 🧾 Essentials (50%) 💸 Wealth (30%) 🎉 Joy & Growth (20%) Why this works: ✅ Step 2: Plan Monthly — Not Daily Budgeting is like a diet. If you track calories every 3 minutes, you’ll quit in 3 days. Plan monthly. Check weekly. Track broadly. Use tools like: ✅ Step 3: Automate the Wealth Bucket This is non-negotiable. Set standing instructions so that: Because discipline is best when it’s automated. 🔁 Budgeting as a Couple (or Family) If you live with a spouse or parents — budgeting is not a solo game. 🫱🏽🫲🏽 Here’s how to align: Make it collaborative, not controlling. 🧘♂️ What Budgeting Actually Gives You Let’s move beyond rupees. What budgeting gives you is: 🌿 Peace — no more wondering “where did it all go?” 🤝 Trust — between you and your partner 🚀 Momentum — because small wins feel powerful 📊 Data — so you know exactly what to fix 💰 Surplus — that’s where true wealth begins 📍 Reflective Journal Prompts (Try Tonight) Here’s how to go deeper. Take 10 quiet minutes. Ask yourself: These aren’t accounting questions. They’re healing ones. 🧱 Brick by Brick: How to Succeed at Budgeting If you take away one thing from this blog, let it be this: Budgeting is not a numbers game. It’s a habits game. And habits are not built in one day. They’re built by showing up again and again. ✅ You’ll mess up a few months. ✅ You’ll overspend sometimes. ✅ You’ll forget to track for a week. But don’t quit. The goal is not perfect budgeting. The goal is peaceful progress. And if you keep showing up, one habit at a time — You’ll become that person who doesn’t just earn money… But directs it like a leader. ✨ Final Word: Your Money Wants Leadership, Not Luck You don’t need to be a finance expert. You don’t need to say no to life. You just need to own your money story. Budgeting is your way of saying: Your ₹50,000/month can create more peace than someone earning ₹2 lakhs — if you lead it well. So start. Start small. Start messy if you have to. Because financial freedom doesn’t start with income. It starts with intentional budgeting.

💑 Money & Marriage: How Indian Couples Can Build Financial Peace Together

Financial peace is not built in one conversation—it’s built over consistent, courageous conversations. ☕ 1. The Silent Stress in Indian Homes The other day, during a 1-on-1 session, a client of mine said something that stuck with me: “Shiv bhai, I earn well. My wife earns too. But when it comes to money… there’s tension. Silence. And sometimes, cold wars.” And it hit me: So many Indian homes are filled with unspoken money stress. From EMI pressures to in-law expectations, from “who earns more” to “why did you spend that much”—Money, though silent, often screams the loudest in relationships. And yet… we rarely talk about it. Not in schools.Not before marriage.Not even during it—unless there’s a crisis. 🧠 2. Why Couples Must Talk Money — Together Marriage isn’t just a union of hearts—It’s also a merging of financial energies. But here’s the truth most couples don’t admit: Love is emotional. But peace in marriage is often financial. You may love your partner dearly,but if you constantly feel unsafe, unheard, or unclear about your shared financial path… That love starts to feel heavy. Because money is not about rupees—it’s about security. It’s about: When that’s missing, even a small money issue becomes a big marital fight. 🛑 3. The Indian Reality: Cultural Silence Around Couple Finance Let’s acknowledge this:In Indian families, money has always been… a little taboo. Your parents never sat and taught you how to manage finances together. Especially in traditional setups: But we’re in a new India. Dual-income households. Aspirational lifestyles. Rising EMIs.And yes—growing emotional distance if money is not handled well. So let’s learn how to shift that. 🛠️ 4. 5 Toxic Patterns That Destroy Financial Peace in Couples Before we build peace, we must identify the patterns that sabotage it. Here are five I’ve seen (again and again): ❌ Pattern 1: One Partner Controls Everything Usually the higher earner. They take all decisions. The other just adapts.This leads to resentment and silent disconnection. ❌ Pattern 2: “I’ll Handle My Money, You Handle Yours” Sounds independent. But in a marriage, it creates parallel lives—not partnership. ❌ Pattern 3: Hiding Expenses “I’ll just buy this and not tell.”This financial infidelity starts small. But erodes trust. ❌ Pattern 4: No Shared Goals You’re rowing the same boat—but in different directions.One wants to save for a home, the other wants to travel. Chaos. ❌ Pattern 5: Money Talks = Only During Crises You only talk money when there’s a problem. That talk is tense, reactive, and defensive. No peace. 🌱 5. The Mindset Shift: From “Me & You” to “Us” The biggest upgrade a couple can make is this: “It’s not YOUR salary or MY loan.It’s OUR financial life.” You’re building a shared journey.That means shared decisions, shared dreams, and yes—shared discipline. Not “who earns more.”But “how can we grow together.” ❤️ 6. How to Start the Money Conversation with Your Spouse Let’s make it practical. Here’s how to gently open this conversation—even if money has never been discussed openly before. 🕯️ Step 1: Choose the Right Mood & Moment Not during a fight. Not when bills are pending.Do it on a calm Sunday, after dinner, with soft music and chai. Start with: “I’ve been thinking about our dreams… and how we can achieve them together.” 🗣️ Step 2: Be Honest About Where You Are Share your income, savings, debts.Ask your partner to do the same.Use a Google Sheet or a notebook. Get real. 🧭 Step 3: Dream Together Ask: Let it be a vision exercise—not a pressure talk. 🤝 Step 4: Decide Roles, Not Hierarchies Decide who manages what—based on strength, not gender. 🧘♂️ Step 5: Create a Peace Plan Agree on: And revisit it once a month, calmly. 📈 7. How to Structure Couple Finances in India (Practically) Here’s a hybrid system I often recommend to couples in coaching: ✅ 1. Three Accounts System: ✅ 2. Income Contribution Based on Ratio: If Partner A earns ₹80,000 and Partner B earns ₹40,000,then for joint expenses, A contributes 66%, B contributes 33%. ✅ 3. Monthly Review Ritual: Pick 1 Sunday/month. Sit together. Review your: Make it fun—snacks, light music, even a reward if you stayed on track! 💎 8. 7 Couple Money Habits That Lead to Peace Let’s go from theory to transformation. Here are daily/weekly habits that lead to long-term financial peace: ✅ 1. Set a Monthly “Money Date” A non-negotiable calendar event. You discuss dreams, not just bills. ✅ 2. Decide Big Purchases Together Set a ₹ threshold. “Above ₹5,000, we decide together.” ✅ 3. Talk About Emotions, Not Just Numbers Ask: ✅ 4. Automate Your Savings & SIPs Let the system work for you. Less stress. More progress. ✅ 5. Build an Emergency Fund Together Start small—₹5,000/month is fine. It’s not just a fund; it’s emotional security. ✅ 6. Use Apps to Track Joint Expenses Use Splitwise, Walnut, or YNAB (You Need A Budget). Make it visual, not vague. ✅ 7. Celebrate Financial Wins Together Saved more this month? Did your first SIP? Hit a debt-free milestone? Celebrate! Go for a dinner. Acknowledge growth. 🧠 9. Reflective Questions Every Couple Must Ask Use these prompts in your next money talk: These questions go deeper than numbers.They touch the heart. They build safety. 🌿 10. Final Thought: Money Is Not a Taboo. It’s a Tool for Togetherness. Dear reader, If you’ve ever avoided talking money with your partner because of fear, guilt, or confusion… Let this blog be your starting point. Because financial peace is not built in one conversation—it’s built over consistent, courageous conversations. You don’t need to be perfect.You just need to be present, honest, and willing. Build a life where: Because a couple that talks money, walks life better—together.

9 Habits to Building Wealth & Be Wealthy from Salary

🌟 1. The Late-Night Truth About Money One day I was sitting alone & silence gave me space to think. “Am I building wealth, or just earning well?” That question hit me like a truck. You see, I’ve coached working professionals who earn 10-15 lakhs a year. But the shocking part? They’re still financially stressed. Credit card bills. EMIs. No savings. And I’ve also met quiet heroes earning ₹30,000 a month who are investing, saving, and steadily building wealth. That’s when it became crystal clear: Wealth isn’t about how much you earn. It’s about what you do with what you earn. 💡 2. The Great Income Illusion We’re conditioned to believe: “A bigger salary means a richer life.” But here’s what really happens: You get a raise. You buy a new car. You switch from Amazon Basics to Apple gadgets. Your rent doubles. Dining out triples. Welcome to lifestyle inflation — the sneaky villain of middle-class dreams. More income. More expenses. Same financial stress. “You’re not broke. You’re just budgeting wrong.” Let that sit. 🤿 3. Why Discipline > Income Let’s imagine wealth as a water tank. Your salary is the water coming in. Your spending habits? The holes at the bottom. You could have the biggest pipe in the colony, but if the holes are bigger, you’ll never store a drop. Discipline is about fixing the holes. Not to live a dry life. But to make sure the water you earn… stays. 📅 4. The 9 Habits That Build Real Wealth Here are 9 habits that have helped my clients (and myself) turn their income into actual, peaceful wealth. ✅ Habit #1: Live Below Your Means No, not miserably. Just mindfully. It’s not about saying no to coffee. It’s about saying YES to future peace. Drive a car you can comfortably afford. Rent a house that lets you sleep without EMI nightmares. Create a surplus. That’s your seed for wealth. ✅ Habit #2: Save Consistently (Even ₹500!) If you can save ₹500/month, you can save ₹5000/month. It’s a muscle. Automate it. Set up an auto-debit the day your salary hits. Pay yourself first. Because if you wait till the month ends… well, you know how that story goes. ✅ Habit #3: Invest Early, Invest Monthly SIPs are not just for finance geeks. They’re for everyday warriors like us. Don’t wait for lakhs. Start with hundreds. Let time and compounding do their job. ✅ Habit #4: Avoid Bad Debt Not all loans are evil. But EMIs for gadgets, vacations, and fancy phones? That’s a trap. You don’t buy the thing. You rent peace to own it. Use credit wisely. Or it will use you. ✅ Habit #5: Track Every Rupee If I gave you ₹1 lakh cash today, would you know where it went in 30 days? Track your expenses. Use a journal. App. Whiteboard. Anything. But know. Clarity is freedom. ✅ Habit #6: Build an Emergency Fund Life throws curveballs. Job loss. Medical bills. Car repairs. An emergency fund (3-6 months of expenses) is your seatbelt. You’ll be glad you had it before the accident. ✅ Habit #7: Know Needs vs. Wants That new phone? Want. Groceries? Need. Most broke people confuse the two. Wealthy people delay the want, never compromise the need. Learn the difference. Live the difference. ✅ Habit #8: Think Long Term Next month’s salary won’t retire you. But 10 years of SIPs will. Plan for your future self. He’ll thank you with a smile, a paid-off house, and peaceful vacations. ✅ Habit #9: Learn Before You Spend Got tempted to buy something? Pause. Ask: “What will this cost me over 5 years?” Learn about where your money goes. Be curious. Read. Ask. Explore. “Financial literacy is self-respect in action.” 🌿 5. Wealth Is Not Luck. It’s Layers of Intentionality You don’t need to be born rich. Or win a lottery. You just need to: Live a little below your means Save a little more than you want to Invest a little earlier than you think And learn a little every single week That’s it. Repeat that for a decade. And you’ll be shocked at what you built. 📍 6. Closing Cue: Ask Yourself This Tonight Before you sleep tonight, ask: “Am I earning to look rich, or building to be free?” If the answer makes you uncomfortable, that’s your first breakthrough. Start small. Start today. Because peace of mind isn’t a product. It’s a habit. And you’re just 1 habit away from wealth. Warmly, Shiv Dwivedi Your Wealth Coach & Financial Freedom Friend

💡Corporate Health Insurance vs. Personal Cover: Do You Really Need Both?

☕ 1. The Late-Night Call That Woke Me Up It was 1:43 AM. My phone buzzed. It was Ravi, an old coaching client and a dear friend. “Shiv bhai… my mom’s in the hospital. Insurance rejected some charges. I thought my company plan would handle everything…” His voice was shaking—not because of the money—but because of the uncertainty. That helpless feeling when something should have worked… but didn’t. We got things sorted. But that night taught both of us something many professionals learn too late: “Just because you have corporate health insurance doesn’t mean you’re fully protected.” Have you assumed that too? 🔍 2. The Illusion of Safety: Why Corporate Cover Feels Enough If you’re a salaried professional, your company probably gives you health insurance. Sounds great, right? You might even think: “It’s already covered.” “Why pay extra?” “I’m young and healthy anyway.” But let’s look deeper. Corporate health insurance is like a raincoat. It works—until the storm turns into a cyclone. And by then, you’re already drenched. 🧳 3. Let’s Talk Metaphor: Travel Insurance at the Airport Imagine you’re going on an international trip. Your airline gives you basic travel insurance—lost luggage, minor delays. But what if: Have you fallen seriously ill abroad? Need hospitalization? Miss 3 connecting flights? That basic plan? Won’t help much. Corporate health cover is like that.It’s helpful, but it’s not built for everything. And worst of all? You don’t control it. Your employer does. 🧠 4. Reflect With Me: Who’s Actually in Control? Here’s a quick reality check: What happens to your cover if you switch jobs? Or worse, if you’re laid off or retire? Will your corporate plan support your parents or dependents fully? Most won’t. Or if they do—it’s limited. Often ₹2-5 lakhs max. So let’s ask the real question: “If a major medical emergency strikes after your job ends, do you have a Plan B?” If your answer makes you pause, good. That pause is awareness. 📉 5. Real Life: When Corporate Cover Wasn’t Enough Let me share a story. Anita, a 38-year-old marketing manager, had ₹3L corporate insurance. Her dad suffered a heart attack. The hospital bill? ₹5.2 lakhs. Her plan covered ₹3L. She borrowed the rest. After that, she decided to buy a personal health cover—just ₹12,000 a year. Small price, big relief. Two years later, she needed surgery herself. This time, she didn’t panic. The policy took care of it. She told me, “Shiv, I sleep better now. I’m not depending on my HR anymore.” That’s peace. That’s planning. That’s power. 📊 6. Quick Comparison: Corporate vs. Personal Health Cover Criteria Corporate Cover Personal Health Insurance Control Employer-controlled You decide everything Coverage Amount Usually low (₹2–5L) Can go up to ₹25L+ Portability Ends with job Fully portable Family Inclusion Often limited You can cover spouse, kids, parents Claim Process Employer-dependent You deal directly with insurer 💬 7. But Shiv, Won’t I Be “Double Covered”? Good question. No. This works to your advantage. In insurance terms, this is called “top-up” or “backup” coverage. Here’s how it works: You use your corporate cover first. If expenses go beyond, your cover takes over. It’s like having Plan A and Plan B—in a world where Plan A often fails silently. 📈 8. Rising Medical Costs — Are You Prepared? Let’s talk numbers: A single hospitalization in a metro hospital can cost ₹5–10L+ A cancer treatment plan can run into ₹25–40L+ A heart surgery costs ₹3–6L+ Daily ICU costs: ₹30,000–₹50,000 in private hospitals Corporate plans often don’t cover: Pre/post-hospitalization Room upgrade charges Experimental procedures OPD, maternity, mental wellness (in many cases) In short, they’re just not enough anymore. 🤝 9. So, What Should You Do as a Professional? Here’s a simple plan: ✅ 1. Keep Your Corporate Cover. It’s useful. No need to cancel it. ✅ 2. Buy a Personal Health Cover. Start with ₹10–₹15 lakhs. Add a top-up if needed.Even ₹10,000–₹15,000/year premiums are worth it. ✅ 3. Include Your Family. Get spouse, kids, and especially aging parents covered. ✅ 4. Buy Early. The younger you are, the cheaper and smoother the process is. ✅ 5. Review Yearly. Add riders. Update the sum assured as income grows. You insure your car. You insure your phone. Why not insure your peace of mind? 🧘 10. Closing Reflection: Health is Wealth. But What About Healthcare? We often say, “Health is Wealth.” But in today’s world, healthcare is expensive.And hoping your HR policy will shield you forever is like expecting your umbrella to withstand a hurricane. Think about it: “If something happened today… are you prepared, or are you just depending on your company?” Your answer could change your family’s future. ❤️ From Shiv’s Heart: Health insurance isn’t about being afraid. It’s about being free. Free from uncertainty.Free from regret.Free to focus on healing, not hustling to arrange funds. Invest in a personal health cover—not just because you can afford it…But because your peace is priceless.

How to Break Free from EMI-to-EMI Living

☕ 1. The Monthly Date I Dreaded It was the 5th of the month. Again. My phone buzzed with the usual barrage of debit messages. “₹12,343 debited — Home Loan EMI.”“₹5,219 debited — Car Loan EMI.”“₹2,750 debited — Phone EMI.”“₹3,499 debited — Personal Loan EMI.” Sigh. I remember staring at my coffee like it would somehow cancel the next notification. “Is this what adulting is all about? Earning to just repay?” I chuckled, but not the happy kind. The chuckle you let out when you feel trapped, but you don’t want to admit it. Ever felt that way, too? 🧳 2. Life in Monthly Installments Imagine life as a suitcase. You’re trying to pack in peace, purpose, health, family time, dreams, joy. But each EMI is like a heavy stone someone keeps throwing in. TV EMI. Sofa EMI. Kitchen EMI.By the time you want to put in something meaningful—there’s no space left. That’s EMI-to-EMI living.You’re not living for yourself—you’re living for your EMIs. It’s not that loans are evil. No. But unchecked EMIs become silent handcuffs. Have you ever looked at your salary credit and felt it vanish before you could even plan what to do with it? 💭 3. The Inner Whisper We All Ignore I remember one evening, my daughter asked,“Papa, can we go for ice cream tomorrow evening?” And I responded with my go-to line: “Let’s see beta, papa has work.” But inside, I was thinking: “I don’t even know if I’ll have the money left by then.” That thought broke me. Not because of the ice cream. But because I wasn’t free. I was earning well, but I didn’t feel rich. I felt restricted. Choked. Like I was running but not reaching. That was my wake-up call. 🔄 4. Why Most of Us Fall Into the EMI Trap Let’s be honest. It doesn’t start as a trap. It starts innocently—”Why pay ₹60,000 upfront when I can pay just ₹2,000 a month?”“EMIs make it affordable,” we say. But then comes the next one. And the next. Before you realize, you’re juggling five balls in the air, hoping none fall. The illusion of affordability slowly becomes the reality of anxiety. It’s like borrowing tomorrow’s peace to fund today’s excitement. And soon, we forget what peace even felt like. 🪞 5. Reflection Time: Where Are You Right Now? Let’s pause. Grab a pen or just close your eyes and think: These are not financial questions. They’re freedom questions. 🧠 6. Breaking Free: The Mindset Shift Here’s what I learned the hard way: The first step to breaking free is not paying off the EMI. It’s understanding why you took it in the first place. Ask yourself: Once you shift from emotion-driven expenses to value-driven choices, you start taking your power back. 🔧 7. The System I Followed to Set Myself Free Let me share the exact 5-step system I used—simple, human, and practical: ✅ Step 1: List all EMIs with interest rates and tenure Most people fear this step. But clarity brings power. ✅ Step 2: Prioritize High-Interest EMIs Personal loans, credit cards—they bleed the most. Tackle them first. ✅ Step 3: Create a “Freedom Fund” A separate savings account just for closing EMIs early. Automate a fixed amount monthly. ✅ Step 4: Consolidate Wisely If you have too many, consider one lower-interest loan to close the rest. But only if you close, not add more. ✅ Step 5: Say No (Even When It’s Hard) Learn to say: “Not now.” A ₹60,000 phone won’t feel good if it brings ₹1,500 stress for the next 12 months. Every EMI you say no to is a “yes” to your future peace. 💡 8. The “Freedom Visualization” That Helped Me Close your eyes for 10 seconds. Visualize a month where: That vision? That’s your why. And it’s more powerful than any budgeting app. 💬 9. A Conversation With My Future Self This might sound funny, but I once wrote a letter to my future self. It read: “Hey, Shiv. If you’re reading this, I hope you said no to that third credit card. I hope you chose freedom over impressing the neighbors. I hope you built wealth that gave you peace. And I hope you remembered: Money is a tool, not a trap.” That letter still sits in my journal. What would your letter say? 👨👩👧 10. One Client’s Journey (That’ll Stay With Me Forever) Poonam, a 33-year-old working mom from Delhi, came to me last year, exhausted. She said, “Shiv, I earn ₹85K/month but have nothing left by the 10th.” We unpacked her EMIs—6 of them. And just like me, she felt “normal” because “everyone has them.” But normal was costing her peace. We worked together: 6 months later, she sent me a message: “I just paid off my personal loan early. I feel like I can breathe again.” That’s real wealth, my friend. 🔁 11. Breaking the Cycle Is Not About Sacrifice. It’s About Choice. People often think: “If I stop EMIs, I’ll have to give up my lifestyle.” No. You’re not giving up your lifestyle.You’re choosing a life with style—peace, dignity, clarity. Wouldn’t you rather wait 6 months for something you can buy in full, than spend 12 months being stressed about something you bought in a rush? 🔚 12. Closing Insight: Real Riches = Emotional Freedom Let’s be real. What you want is not just a zero on the credit card. You want to feel safe. Empowered. Calm. Able to look at your child, your partner, or even your mirror and say: “I’m not surviving anymore. I’m building. I’m choosing.” Money is powerful. But clarity is power.And peace of mind is the real ROI. 💬 Final Reflective Cue: Grab a cup of chai tonight. Sit with yourself and ask:“Which EMI is costing me more than money?” And when you get that answer, promise yourself:“I will start walking out of this loop—step by step, month by month.” You don’t need to do it overnight. But you do need

The 1% Money Habits That Wealthy Never Ignore

Ah, retirement. The very word conjures images of endless sunny days and newfound freedom. But for many, the path to this idyllic future is shrouded in misconceptions, leading to procrastination and regret. Are you telling yourself, “I’ll start saving next year,” or “My pension will take care of everything”? These common myths can derail your dreams. Discover the unshakeable truths about retirement planning, the power of compounding, and the essential investment vehicles that can help you design your freedom years. Your future self will thank you for the choices you make today. Start sketching your masterpiece now!

Smart Money Management: How to Escape the Middle-Class Trap and Build Lasting Wealth

A personal budget is a structured financial plan designed to track your income and expenses over a specific period, typically monthly or weekly.

Beyond the Beach: Debunking Retirement Myths and Designing Your Freedom Years

A personal budget is a structured financial plan designed to track your income and expenses over a specific period, typically monthly or weekly.